Seeking out great stocks to buy is essential, but many would say it’s even more important to know which stocks to steer clear of. A losing stock can eat away at your precious long-term returns. So, figuring out which stocks to trim or get rid of is essential for proper portfolio maintenance.

Even the best gardens need pruning, and our team has spotted a few stocks that seem like prime candidates for selling or avoiding. Continue reading to find out which three stocks our team is staying away from this week.

After reporting mixed Q4 earnings and issuing lower than forecast 2022 guidance last week, Roku shares plunged more than 22%. With Roku’s price nearly 80% off of its July ATH, eager investors may see a buying opportunity here. Considering the obstacles that the not-yet-profitable company is up against, we beg to differ.

The supply chain disruptions that hampered growth in the U.S. television market in 2021 will likely persist well into 2022. “Overall TV unit sales are likely to remain below pre-Covid levels, which could affect our active account growth,” Anthony Wood, Roku’s founder, and CEO wrote in the company’s letter to shareholders. “On the monetization side, delayed ad spend in verticals most impacted by supply/demand imbalances may continue into 2022.”

Roku ended the third quarter with 56.4 million active user accounts, up 1.3 million from the prior quarter. However, analysts had expected 1.68 million new user accounts. Roku said it sees revenue of $720 million for the first quarter, which implies 25% growth. Analysts were projecting revenue of $748.5 million for the period.

Pivotal Research was one of several firms to decrease its rating on Roku on Friday. Analyst Jeffrey Wlodarczak downgraded the stock from Hold to Sell and slashed its price target to $95 from $350. “The bottom line is with increasing competition, a potential significantly weakening global economy, a market that is NOT rewarding non-profitable tech names with long pathways to profitability, we are reducing our rating on ROKU,” the analyst wrote in a note to clients.

Leading medical technology company Medtronic Inc. (MTD) makes our list of stocks to avoid ahead of its Q4 earnings call, slated for Tuesday, February 22nd, before the bell. The company’s fourth-quarter was wrought in turmoil. Medical device recalls drew FDA attention to Medtronic’s California facility, leading to a warning letter about the inadequacy of specific medical device quality system requirements in the areas of risk assessment and corrective and preventive action.

We don’t expect any shockingly positive revelations to be revealed during this week’s call. When we last heard from Medtronic during the year-end call with management and analysts, management said it was too soon to predict the warning letter resolution timeframe, following up with a vague outlook for potential FY22 and 23 sales impact.

JPMorgan analyst Robbie Marcus recently downgraded Medtronic to Neutral from Overweight with a price target of $105, down from $130. The analyst also removed the shares from the firm’s Analyst Focus List citing pipeline setbacks that “complicate” Medtronic’s turnaround. With setbacks to the company’s most significant pipeline products, renal denervation, 780G, and Hugo, management “has work to do to resolve these issues and prove to investors it can execute this turnaround story,” says the analyst. Marcus now views Medtronic shares as fairly valued.

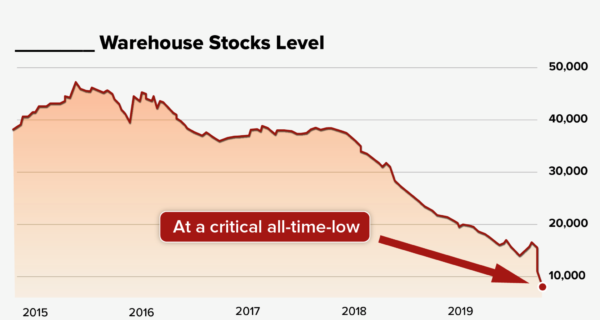

Finally, global supply constraints continue to drag Bed Bath & Beyond (BBBY) sales lower, while inventory replenishment delays are expected to continue well into 2022. BBBY was unable to meet demand in Q3, leading to misses on the top and bottom lines. Management estimates missing out on $100M of sales for the quarter and admits that the company’s turnaround is taking longer than anticipated.

Mark Tritton, Bed Bath & Beyond’s President and CEO, said, “During a quarter where our sales momentum was not where we wanted it to be with sales of $1.9 billion, and a 7% comp decline, improved momentum in November and strong gross margins demonstrated progress in our transformation. After our previously announced slower start to sales in September and October, we drove a change in trends by November, with our comp decline improving, particularly in stores. However, overall sales were pressured despite customer demand due to the lack of availability with replenishment inventory and supply chain stresses that had an estimated $100 million, or mid-single-digit, impact on the quarter and an even higher impact in December.”

As a reflection of the continued impact of anticipated global supply chain challenges, the company lowered its Q4 guidance. BBBY now expects EPS of $0 -$0.15 and Q4 revenue of $2.1B. The revelation sent waves through the analyst community, where revenue of $2.27B and 72c EPS is expected for the fourth quarter.

Loop Capital analyst Anthony Chukumba lowered the firm’s price target on BBBY to $10 from $14 and kept a Sell rating on the shares. The analyst tells investors in a research note that the company’s Q3 went “from bad to worse” with “substantial” misses on revenue, profitability, and earnings. Chukumba adds that he continues to believe that Bed Bath’s struggles are largely because the company has lost market share and consumer relevance, neither of which will be “easy to regain.”

We’re sticking to the sidelines while the company pursues additional expense optimization measures.