Any given investor’s current objective, one’s statistics-based financial situation should play a major role in determining which stocks are the best to introduce to their portfolio— and remember: stocks that already exist in your portfolio should also be considered. “Will these stocks get along with each other?” That might be a bit of a joke, and this also might be rhetorical advice. I think it’s okay to reiterate the sentiment to keep it at the forefront of our brain’s financial lobe. It’s vital right now to utilize the best guidance you can receive when it comes to making ideal financial decisions.

Although I mostly talk about stocks (which we’ll get to in a few more seconds), I’m assuming my readers already know that it’s not always just about the tickers we hold stock in, and there are other things to consider. For example, an expert might tell us it’s wise to set up an emergency fund separate from our regular savings accounts. It’s also a good idea to divide up our assets and know when to invest in a particular area of the market, in and around where there is certainly money to be made.

As a long-term investment, I think these equities work well, especially given that some analysts’ forecasts feel bleak; we’re experiencing inflation as the Fed is hiking rates, and we aren’t exactly miles away from some type of recession. It’s possible. Personally, I’m not a future teller, nor am I Warren Buffett. However, I am very much “kept up,” if you will — I try to remain an optimist, too — and so I humbly ask you to look at these stocks I happen to like. Let’s not focus too much on sectors or industries right now. In this case, we have a retailer, a home improvement/trade firm, and one from the financial sector. That’s not the point of today’s list, which is simply about three strong stocks to watch and consider.

That said, I’ve considered overall stock performance as usual, and although analysts are sometimes split, it’s only between buy and hold. These are strong equities. Let’s have a look:

TJX Companies Inc (TJX)

TJX Companies Inc. (TJX) operates HomeGoods stores,Marmaxx stores, and, internationally, TJX stores. TJX’s primary focus of operations is dealing in clothing and household TJX International, based in the U.S., runs TJX‘s locations. TJX was founded by Bernard Cammarata in 1976 in Framingham, MA, where its headquarters remain. With its stock down YTD only slightly by 0.83%, TJX has been performing well; it has a market cap of $90.6 billion and a decent beta score of 0.91. TJX shows TTM (trailing twelve-month) revenue of $50 billion, from which it profited $3.5 billion with an even 7% net margin. TJX has a forward P/E (price to earnings) of 22.5x, a P/S (price to sales) ratio of 1.85x, and a PEG (price-earnings-growth) ratio of 1.93x, with an ROE (return on equity) of 56.57%. With almost $2 billion in free cash flow, TJX has a 10-day average trading volume of 4.09 million shares. TJX has a dividend yield of 1.68%, a quarterly payout of 33 cents ($1.32/yr) per share, and a payout ratio of 38.55%. Analysts have marked TJX with a median price target of $88, with a high of $95 and a low of $75, representing a potential 20% or higher jump from its recent price. TJX has 17 buy ratings and 7 hold ratings.

Realty Income Corp. (O)

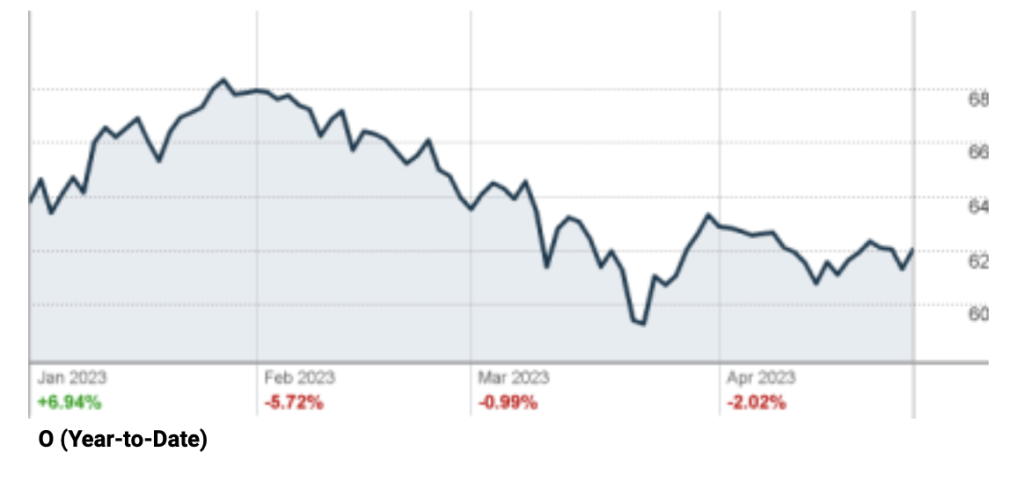

Realty Income Inc. (O) is a real estate business that, particularly given its recent pricing, pays decent monthly dividends thanks to a steady income stream. O‘s headquarters are in San Diego, CA, and it was founded in 1969 by William E. Clark, Jr., and Evelyn Joan Clark. O’s stock is down YTD by a slight 2.19% and sits at the bottom of its existing 52-week range, making for a good opportunity considering its profitability as a stock. O has a market cap of $41.2 billion, an enterprise value of $60 billion, a safe 0.80 beta, and an impressive recent track record versus analysts’ earnings projections; O, for the last two fiscal quarters, exceeded Wall Street’s EPS forecasts most recently by 12.08% and 18.86% the quarter prior. O reports $3.3 billion in TTM revenue with a $1.42 per share EPS, profiting $870 million with a net margin of 26.01%. O has a free cash flow of $1.54 billion and a 10-day average trading volume of over 3 million shares. O has a dividend yield of 4.91%, with a quarterly payout of 76 cents ($3.04/yr) per share via a generous payout ratio of 209%. Analysts give O a median price target of $70, with a high of $74 and a low of $65. This will make more sense when looking at the chart below; even the forecasted range’s lowest price would give the stock a 5% jump from current pricing. O has 9 buy ratings and 7 hold ratings.

Floor & Decor Holdings Inc. (FND)

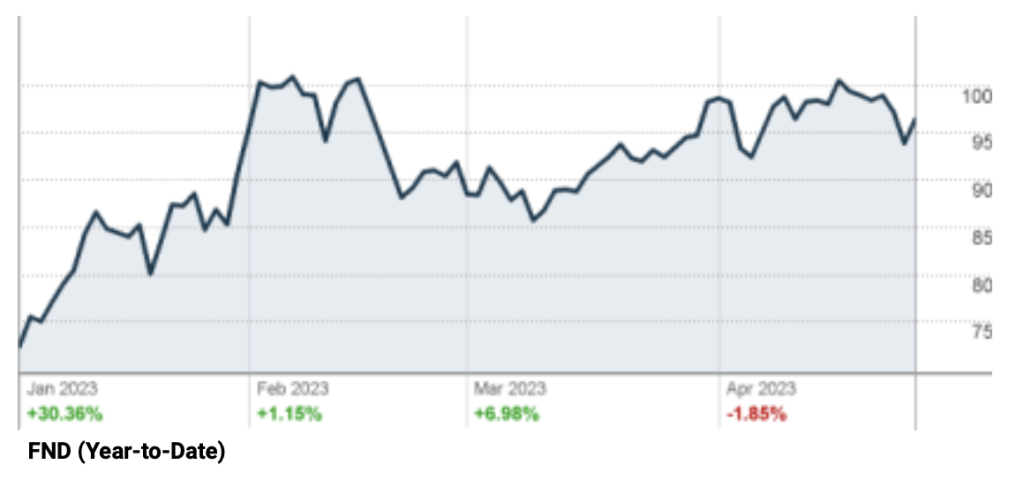

Floor & Decor Holdings, Inc. (FND)’s primary business activity is the sale of hard surface flooring and accessories. Flooring materials such as wood, stone, vinyl, laminate, and tiles are among its many offerings, and FND also offers installation services. George Vincent West founded FND in 2000, and its headquarters are in Atlanta, GA. Stock-wise, FND is flying pretty high at the moment, so now would definitely be the time to get a piece of it; the stock is up by 38.45% YTD and, with upside, has time yet to continue trending upward. FND has a market cap of $10.4 billion, a 1.86 beta that might just have to be worth the risk (there’s volatility everywhere), an ideal ROE (return on equity) percentage of 20%, and a healthy D/E (debt to equity) of 24.60%. FND shows TTM revenue of $4.26 billion at $2.79 per share, from which it profited $300 million on a 6.99% net margin. FND shows remarkable YOY (year-over-year) growth in all reported areas and has beaten analysts’ EPS projections for the last four consecutive earnings seasons, in reverse order, by margins of 11.95%, 8.17%, 3.74%, and 2.92%, respectively. With a current 10-day average trading volume of 1.3 million shares, the analysts who offer yearly price projections have weighed in, giving FND a median price target of $98, with a high of $120 and a low of $73. This range gives FND a potential upside of 24.50%. FND has 13 buy ratings and 9 hold ratings.

Read Next – Protect Yourself from Biden’s Dollar Destruction…

Take a look at this:

What I’m holding in my hand is a completely new form of money…

As we speak, it’s being used as an alternative currency across the U.S. minting in places like Utah, New Hampshire and Nevada…

And since it’s made out of a thinly printed sheet of REAL gold…

It may be the single best way to protect your wealth from a sinister plot by president Biden to completely DESTROY your money.

Because rest assured…

Biden has already set the stage for a government-controlled digital dollar – which I believe is a DIRECT threat to your wealth and financial security.

That’s why I’m sounding the alarm about this important new form of money called a “Goldback”…

And why I want to get your hands on it right away.

There’s just one catch.

Since I have a limited number of these…

I need you to respond to this message immediately.

If you don’t, you may miss out on this opportunity forever.

I’ve recorded a short 2 minute message that explains everything here.

Including what this new money is, why it’s so important that you have some, and how to claim yours right away.