Seeking out great stocks to buy is essential, but many would say it’s just as important to know which stocks to steer clear of. A losing stock can eat away at your precious long-term returns. So, figuring out which stocks to trim or get rid of is an important part of proper portfolio maintenance.

Even the best gardens need pruning and our team has spotted a few stocks that seem like prime candidates for selling or avoiding. Continue reading to find out which three stocks our team is staying away from this week.

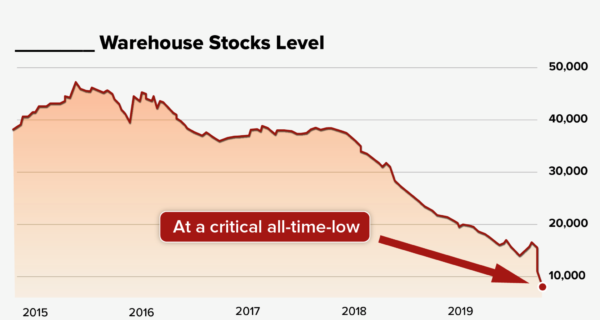

Offshore oil rig service provider Transocean (RIG) suffered badly in the wake of 2020’s economic shutdown and travel bans (when crude prices plummeted to all-time lows), but the company was in bad shape long before that. In 2019 prior to the pandemic, Transocean reported an EPS loss of $1.45. Bank of America analyst Mike Sabella projects that losses will continue through at least 2023.

He’s projecting Transocean will finish 2021 with about $450 million in liquidity, and the company will generate negative $50 million in 2022 free cash flow. Bank of America has an Underperform rating and $1 price target for Transocean. Considering that Transocean has more than $8 billion in debt and $600 million in 2022 debt maturities, Sabella’s forecast doesn’t seem unrealistic.

The current consensus among the 15 analysts offering recommendations is to Hold RIG. The stock has 10 Hold ratings, 5 Sell ratings and no Buy ratings. A median target of $3 represents a 25% decrease from the most recent price.

For the third quarter of 2021, this offshore drilling contractor expects adjusted contract drilling revenues of $670 million, indicating growth from the sequentially reported figure of $656 million. It expects third-quarter operations and maintenance expenses of $427 million. Its G&A expenses are expected to be $40 million while capital expenditure including capitalized interest is estimated to be $90 million.

Gold is in a strange moment in its history, and it has everything to do with cryptos. Wall Street is providing as much exposure to cryptocurrency demand as investors can handle. Cryptos are now the preferred alternative investment over gold.

Gold has been trading in range for a while now and gold producers have gotten stuck as well. The pandemic has slowed operations and demand and now the market is feeling the delta wave’s strain on gold demand and production.

This could all change at some point, if the markets ever correct. But for now gold has taken the back burner and gold miners are not faring well.

Canada-based Barrick Gold Corp (GOLD) made it to our stocks to sell or avoid list because currently, it isn’t attracting buyers and gold prices aren’t going anywhere. GOLD has lost nearly 9% in the past 3 month and 30% in the past year.

Verizon’s (VZ) average analyst price target has decreased by around 60 cents in the past six months. It’s also concerning that VZ’s average broker recommendation has decreased by 0.28 in the past eighteen months and is currently just 2.7 (Hold); 19 analysts consider the stock a Hold, only 7 consider it a Buy, and 2 consider VZ a Sell.

VZ may seem to have an attractive beta for those seeking growth with low risk, but now is not the time to buy VZ. The stock’s price returns are disappointing to say the least. The problem with VZ isn’t lack of demand for their internet and cable service, it’s accessibility. Millions of consumers are willing to pay for VZ’s services but simply do not have access.

Verizon stock is down more than 11% YTD versus a 21% rise in the S&P 500 during the same period.