Seeking out great stocks to buy is essential, beyond a doubt, but it’s just as important (if not more important) to know which stocks to steer clear of.

A losing stock can eat away at your long-term returns. So, figuring out which stocks to trim or get rid of is integral to proper portfolio maintenance.

Even the best gardens need pruning, and our team has spotted a few stocks that seem like prime candidates for selling or avoiding. Continue reading to find out which three stocks made it to our list this week.

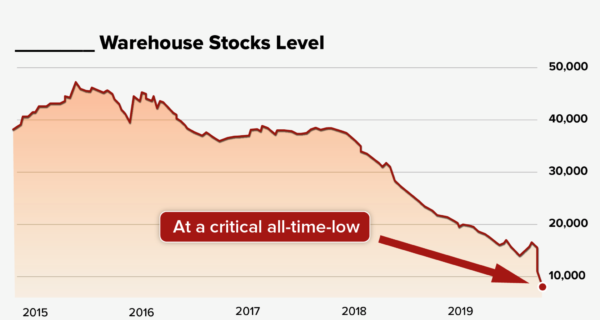

First up on our list of stocks to avoid is Big Lots (BIG). The company’s challenges include supply chain bottlenecks, increasing freight expenses, labor challenges, and competition in food-/consumables.

On Tuesday, Piper Sandler analyst Peter Keith downgraded Big Lots to Neutral from Overweight, saying in a note to clients that the economic environment was turning sour for the retailer.

“We see a trifecta of macro headwinds impacting fundamentals through the first half of 2022,” Keith wrote.

“These include the end of two years of stimulus check tailwinds in next year’s first half; ocean freight rates continue to intensify to all-time highs and are likely a gross-margin drag through the first half of 2022, and retail industry wage pressure seems unlikely to materially abate any time soon,” he added.

Big Lots missed Wall Street estimates for earnings and revenue when it reported its second-quarter results in August. For the quarter ended July 31, the company reported earnings of $37.7 million, compared to $452 million in the year-earlier quarter, according to the earnings release. Revenue declined to $1.45 billion, compared to $1.64 billion reported a year earlier.

The stock has been on a significant descent, dropping almost 30% over the past three months. Piper Sandler lowered its price target on the stock to $50 per share from $60. That’s 7% above where shares of Big Lots closed on Friday.

Next up is the aerospace and defense technology company, L3Harris Technologies Inc. (LHX). The company provides defense and commercial technologies across air, land, sea, space, and cyber domain. In the past six weeks, LHX stock has seen a downward trend in fresh estimates and bled nearly 5% in the same time period. Some analysts think the stock has more to lose.

Among analysts who have recently downgraded the stock is Goldman Sachs’ Noah Poponak, who downgraded the stock from Neutral to Sell. Poponak told investors in a note on Thursday, “A deceleration in the U.S. defense budget growth rate will likely translate to a multi-year deceleration in L3Harris sales.” He added, “Margin upside that was driven by merger integration has now likely played out, leaving less upside to margin estimates.” With the stock significantly outperforming its large-cap defense peers over the last six months, the analyst no longer sees a “relative valuation gap” in the stock.

The company also recently lowered its 2021 guidance range. L3Harris currently expects to generate revenues of $18.1-$18.5 billion, compared with the prior guidance range of $18.5-$18.9 billion, during 2021. The company’s 2021 earnings are now projected to be in the range of $12.80-$13.00 per share, compared with the previous guidance of $12.70-$13.00.

Last, on our list, we have a stock that has recovered and then some. One area that has done exceptionally well in the wake of the pandemic is the online used car market. While pandemic shutdowns eliminated many of its brick-and-mortar used car peers, Caravana (CVNA) thrived.

Since March 2020, CVNA’s share price has bolted upward 12x. So far in 2021, Carvana has shot up another 50%, almost tripling the performance of the S&P 500.

Still, Carvana isn’t substantially profitable, and the company’s recent $750 million debt issuance shows its cash-bleeding nature. Not to mention that the stock is downright expensive right now. CVNA’s current share price reflects a market cap of more than $60 billion, which puts Carvana at a higher value than Ford (F) on a market cap basis.

When you consider the company’s enterprise value (that is, the company’s market capitalization plus all its net cash or debt position), Carvana is roughly 5x more expensive than its closest rival, Vroom (VRM), which is smaller and growing at a slower pace, but that valuation seems unrealistic. While we do see a promising future for the industry, we’ll let Carvana cool down for a while before considering it in the buying range.